Leveraged Buyout (LBO) Primer

Understanding Leveraged Buyouts (LBOs):

Leveraged buyouts (LBO) are a type of acquisition where investors finance the purchase of a target company via debt financing (usually 50-60% is debt financing and 40-50% is equity).

In an LBO, the investors seek to increase the target company’s revenue and EBITDA in order to pay down debt and increase the total value of the company, driving outsized increases in equity value before selling the company or executing an IPO.

LBOs have several benefits, such as: allowing firms to acquire larger companies than they could with equity alone, facilitating ownership transitions, allowing founders/owners to retain a stake and participate in future value creation, and strong returns for equity investors. However, they also carry significant risks, including elevated borrowing costs in a higher interest rate-environment, risk of credit default, and reduced cash available for other corporate purposes, including investing in future growth.

A successful LBO requires experienced advisors who understand the importance of a suitable target company, current market conditions, and how to navigate the complicated process.

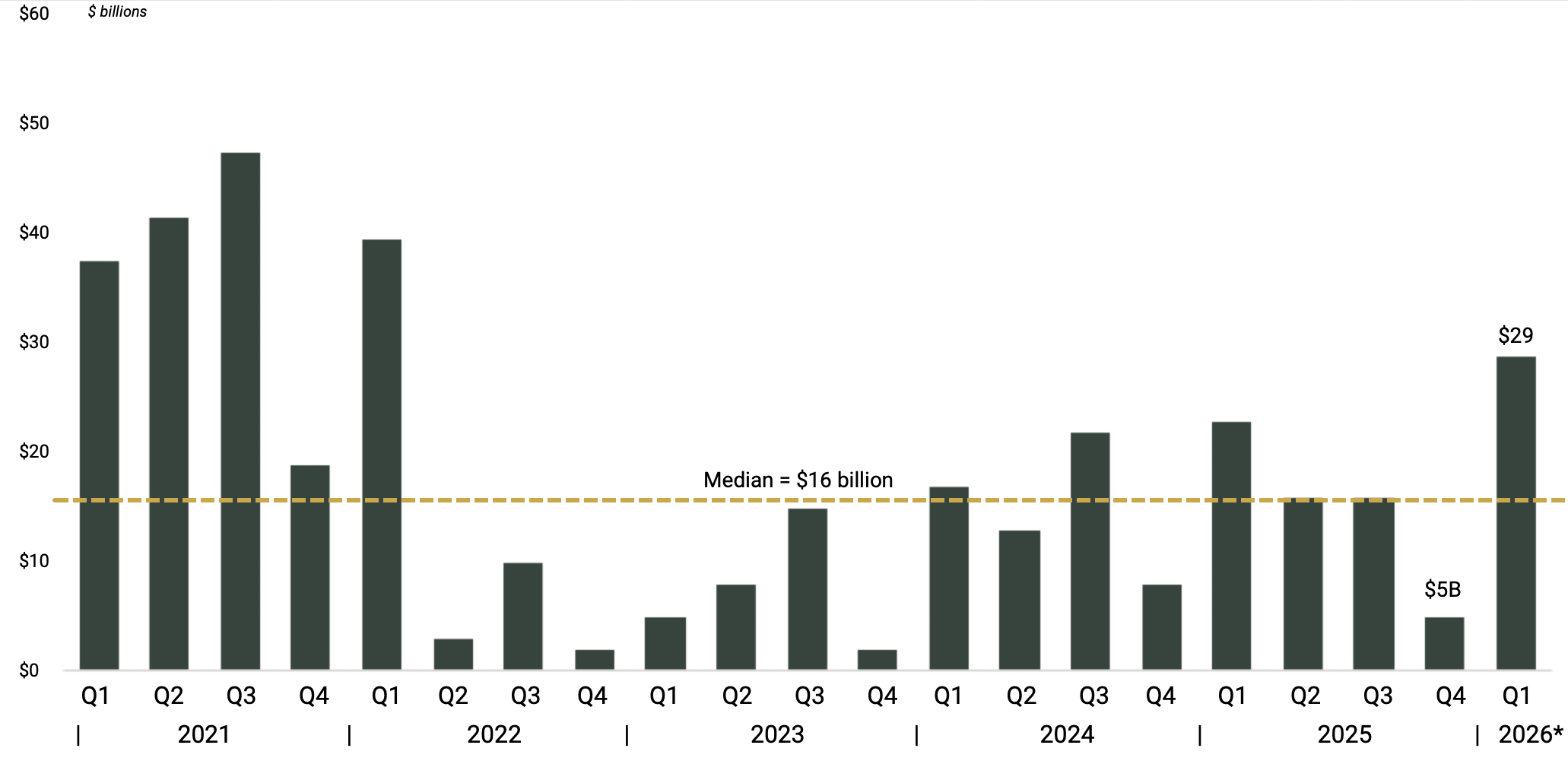

Volume of LBO Loans Issued for Institutional M&A

Source: Pitchbook, Ropes & Grey, 2026 represents YTD through 03.31.2026

What is a Leveraged Buyout?

A leveraged buyout (LBO) is a type of corporate acquisition where the buyer, usually a financial investor or a group of investors, funds a significant portion of the purchase using debt capital. The buyer typically borrows 50-60% of the purchase price, using the target company’s assets as collateral for the borrowed capital and the cash flow from the target to repay the debt over time. The buyer contributes the remaining 40-50% of the purchase price as equity capital.

The acquired company (often referred to as the “target” of the LBO) may include public and private companies, family-owned businesses, or divisions of larger firms with stable cash flows, strong market positions, high growth potential, and a proven management team. The buyer will look for the target company to have a clear exit strategy within three to five years. The investment thesis for an LBO buyer is that, as an investor, they can earn a financial return by boosting the equity value of the target company through debt reduction and earnings growth. Equity investor targets for an LBO are often as high as 18%+ annual or internal rate of return (“IRR”) and 2.0+ times cash-on-cash return.

Investors generally have a three- to five-year holding period and then seek to monetize their investment by selling the target company, recapitalizing through the payment of dividends, or through a public stock offering called an Initial Public Offering (“IPO”). More recently, the hold periods for LBO investors has been much longer than the three to five years, however investors are still underwriting new deals with the shorter than expected hold period.

LBO activity has historically been strongest when borrowing costs are low and corporate valuations are moderate. These conditions prevailed for much of the 2010s, when interest rates were low. However, the more recent recovery in deal activity demonstrates that debt-financed buyouts can remain viable even in a higher interest rate environment.

Free LBO Model Template

Built in Excel - quickly model and analyze your LBO transaction.

How Do Leveraged Buyouts Work?

Here are the general steps taken in an LBO - from the initial interest in the target LBO company to dispersing funds after the target LBO company is sold:

Identification of the Target LBO Company: The private equity investor or family office identifies a potential LBO target. The primary requirement for an LBO target is the ability to support debt repayment. Good indicators of a suitable target are a company with stable cash flows, a strong market position, quantifiable growth potential, and a capable management team.

Structuring the Deal: Once the buyer has identified the target, they approach lenders to secure debt financing. Each acquisition is unique, and the deal’s structure will depend on several factors. Typically, 50-60% of the purchase price is funded through debt. The buyer funds the remaining portion of the purchase price as equity from private equity funds or from co-investors. Co-investors can come in the form of other private equity firms that form a consortium to purchase the company, or from existing limited partners in a private equity fund that will invest additional capital in individual transactions. Co-investors allow private equity firms to acquire larger targets than they might otherwise be able to acquire on their own and diversify risk.

Acquisition and Ownership: The investors acquire the LBO target company using the combined funds from debt and equity. After the acquisition, the investors may choose to reorganize the company to improve efficiency, cut costs or implement strategic changes. Often LBO investors will explore acquisition opportunities as a pathway to accelerate growth.

Repaying Debt: As the LBO target company generates cash flow from operations, investors use a portion of the cash flow for debt repayment, thereby increasing the LBO target company's equity value.

Exit Strategy and Returning Funds: Investors aim to exit the LBO target company in three to five years (although it often takes longer) by selling it to another buyer, taking it public through an IPO or conducting dividend recapitalizations. Once the company is sold or another shareholder liquidity event occurs, funds are returned to investors.

Leveraged Buyout Deal Volume and Market Share

In Q1-2026, leveraged buyouts made up the majority of acquisition financing as measured by volume of institutional loans issued for M&A transactions. As illustrated in the chart above, the volume of LBOs can fluctuate on a quarterly basis, with the median volume of $16 billion per quarter from 2023-2026.

Private Equity Leveraged Buyout

Private equity (PE) firms frequently use leverage to enhance equity returns for their fund investors, similar to how investors buy stock on margin or purchase real estate utilizing debt or a mortgage. PE firms form fixed-life limited partnership funds that pool committed capital from limited partners (LPs) such as pension funds, high-net-worth individuals, family offices, endowments, and other institutional investors. These funds use leverage to amplify returns while managing financial risks through reliable cash flows.

A typical private equity fund has a ten-year term:

Initial four to six years: This is the “investment period,” when firms acquire target companies, leveraging their experience and expertise to restructure, grow, and enhance the value of the companies in their investment portfolio.

Next four to five years: After the investment period is the “harvest period.” During this time, the private equity firm monetizes its investment portfolio via recapitalizations, selling to other buyers, executing an IPO, or through a secondary stock sale. Upon a liquidity event, proceeds are returned to the limited partners who contributed to the private equity fund.

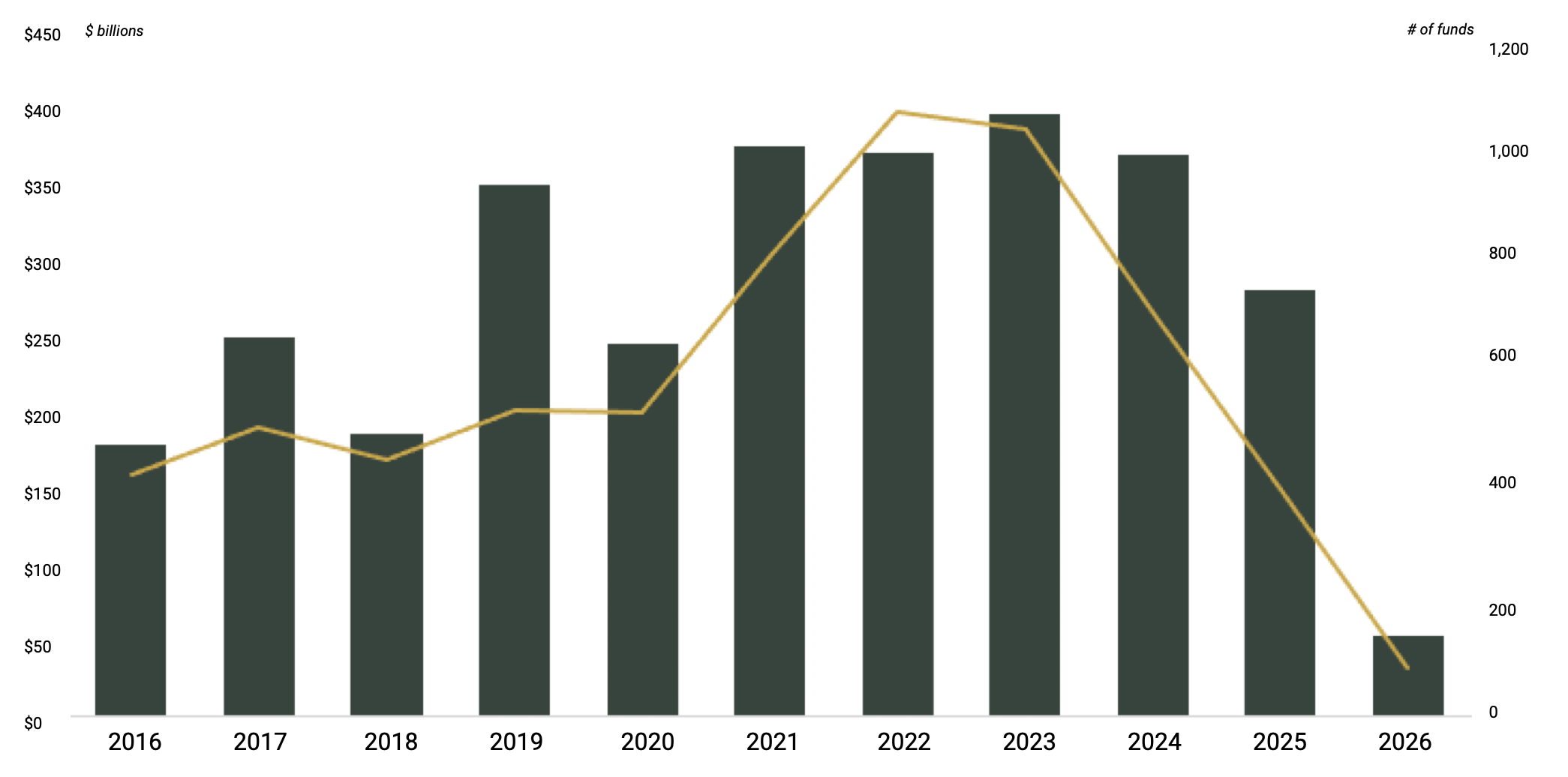

Private Equity Fundraising

Source: Source: Pitchbook, 2026 represents YTD through 03.31.2026

PE firms are compensated primarily via annual management fees (~2%), a share of profits on their investment portfolio (~20%), and any associated transaction or monitoring fees. Funds often focus on specific investment sizes, industries of expertise, or specific corporate growth stages where they can leverage specialized knowledge to identify and execute LBOs, thereby maximizing returns for investors.

Family Offices (Direct Investing)

Single-family and multi-family offices are often limited partners in private equity funds, but they are increasingly becoming more active in directly investing in LBOs. When participating as direct investors in these transactions, family offices often have fewer restrictions on their holding period and less defined guidelines on the timing of capital returns. Where PE funds aim for an exit on their LBO within three to five years as described above, family offices generally have a longer-term investment horizon. They may specialize in industries where the family has experience, deep knowledge or history. More recently, family offices have emerged as meaningful participants in co-investments alongside PE sponsors.

Types of Leveraged Buyouts

There are different types of LBOs, all of which have different goals, investors, and financing structures. Some common types of LBOs are management buyouts, secondary buyouts, and take-privates.

Leveraged Management Buyout

A management buyout (MBO) is a financial transaction in which an individual from the corporate management team or the entire team purchases the business from the original owner using a mix of borrowed capital, personal resources, and private equity investors. Buyers utilize this type of buyout to take a publicly traded company private or to acquire a private company from existing owners. The appeal of MBOs is that they provide management with more control of the business and greater opportunities for financial rewards.

Secondary Buyout

A secondary buyout occurs when one investment firm acquires a target LBO company from another investment firm that initially acquired the company via an LBO. Secondary buyouts are attractive because they provide the seller firm with instant liquidity and make room for other M&A activities. Historically perceived in a negative light, secondary buyouts are a good option when the seller firm has already realized significant gains from the investment and/or the target company would improve under a different firm’s management.

Take-Private

A take private LBO occurs when a company or group of investors seek to acquire a publicly traded target company, often in concert with thetarget company’s management team, and de-lists the company so it is no longer publicly traded. Other than the public to private nature, these transactions follow a similar path as a typical LBO.

The Advantages of Leveraged Buyouts

LBOs offer several advantages, primarily centered around financial efficiency and value creation. By using debt to finance a significant portion of the acquisition, investors can amplify their potential returns on equity, making LBOs a powerful tool for enhancing investment performance. Using leverage allows firms to acquire larger companies than they could with equity alone, enabling access to valuable assets and markets. Additionally, the debt obligations create a disciplined management environment focused on cash flow and operational efficiency, often leading to cost reductions and improved profitability. LBOs also provide opportunities for restructuring and strategic realignment, unlocking hidden value and driving long-term growth. For investors, LBOs offer the potential for high returns while diversifying their portfolios with substantial, asset-backed investments.

Risks Associated with Leveraged Buyouts

While the LBO model has several benefits, there are also significant risks. Potential investors should evaluate the current market conditions and their capacity to take on debt. Some of the risks include:

High-interest payments are associated with the leveraged loans, high-yield debt, and mezzanine (a hybrid debt and equity financing option) financing of LBOs. Lenders often charge higher rates to offset the increased risk of leveraged buyouts.

Increasing borrowing costs in a rising-rate environment: LBO debt often includes floating-rate debt, tied to a benchmark interest rate (most commonly SOFR) plus a spread. In a rising-rate environment, the cost of servicing debt payment can rise significantly, straining lending covenants and cash flow.

Pressure on cash flow due to substantial debt repayment obligations can reduce operating flexibility and limit a target LBO company’s ability to capitalize on growth opportunities. These pressures can be exacerbated by changes in market, competitive and economic conditions.

Excessive debt can lead to a lower credit rating, making it challenging to secure new financing. This can potentially hinder the target company’s ability to undertake new projects or expand its portfolio.

To justify an LBO, the target LBO company must demonstrate strong cash flow and profitability, ensuring that the anticipated profits from the acquisition will outweigh the costs of high-interest loans. Proactive planning and contingency measures are essential to mitigate these risks and manage the financial burden effectively.

Leveraged Buyout Example

Below is an example of a leveraged buyout transaction (the “Illustrative LBO”), demonstrating the typical structure and mechanics in a conventional leveraged buyout scenario. The Illustrative LBO assumes a company with $25 of earnings before interest, taxes, depreciation and amortization (“EBITDA”) is acquired for 8.0 times EBITDA, implying a total transaction value of $200. The $200 transaction value is funded with $120 of new debt (representing 4.8 times EBITDA and 60% of the total purchase price) and $80 of new investor equity (40% of the total purchase price). Investors use proceeds to repay the existing debt of the target company, and the remaining $180 is used to purchase all of the equity interests from existing shareholders.

Note: Buyout Investors often require management and, in some cases, existing investors to roll over a portion of their existing equity interest into a new equity investment.

In this example, the investors focus on strategies to grow revenue and EBITDA and then target the end of year five to exit the company. During years one through five, the target grows revenue and EBITDA. The buyers use cash from operations to pay interest expense and principal on the $120 of debt to fund the purchase.

In Year 5, the company, which is now generating $31.9 of EBITDA, is sold at an 8.0 times EBITDA multiple, valuing it at $254.8. After repaying $68.2 of the remaining debt, the remaining equity value is $186.6.

Based on an initial investment of $80, the equity holders have earned a 2.3x “cash-on-cash” return (implied equity value / initial investment) and a compound annual return or internal rate of return (“IRR”) of 18.5%.

NOTE: This is an example scenario and does not represent any Keene Advisors’ clients or other organizations

The Bottom Line

Leveraged buyouts can be a good strategy if the conditions are right and the investors have done their due diligence to ensure the LBO target company meets specific requirements. An LBO is also a possible exit strategy for founder- and family-owned businesses that have previously raised venture capital funding or have been self-funded. Understanding an LBO's mechanics, benefits, and risks can yield positive results. They also require strong advisors who can educate management teams on the risks and rewards of an LBO, detail subsequent operational and cash flow requirements, and handle the due diligence and management of the acquisition process.

Keene Advisors is a full-service independent investment bank and strategy advisory firm built for private, founder, and family-owned businesses. Our team has advised on over 200 investment banking and strategy consulting engagements over the last 25 years, including over $45 billion in mergers & acquisitions, leveraged buyouts, capital raising and restructuring advisory transactions.

We are dedicated to transparent communication and seamless guidance throughout every stage of the process, always aiming to align short-term needs with long-term goals.

Contact us today for a confidential consultation on leveraged buyout transactions or other corporate finance and M&A considerations.

Investment Banking

& Strategy Advisory

Built for Private, Founder,

and Family-Owned Businesses

Disclaimer: This commentary is intended for general informational purposes only. Keene Advisors does not render or offer to render personalized financial, investment, tax, legal or accounting advice through this report. The information provided herein is not directed at any investor or category of investors and is provided solely as general information. No information contained herein should be regarded as a suggestion to engage in or refrain from any investment-related course of action. Keene Advisors does not provide securities related services or recommendations to retail investors. Nothing in this report should be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product. Securities offered through Burch & Company, Inc., member FINRA/SIPC.