Q1-25: M&A Activity Stalling Amid Market Uncertainty

M&A activity showed signs of recovery in late 2024, but market uncertainty in early 2025 has stalled deal momentum. Despite declining borrowing costs and a record $2.6 trillion in private equity dry powder, investor hesitation has grown due to unpredictable trade and economic policies. Companies considering a sale should focus on financial preparedness and operational efficiencies to position themselves for success when dealmaking accelerates.

From Raising Capital to Generating Returns: The Private Equity Fund Lifecycle

Private equity funds serve as a critical source of capital for business owners seeking liquidity or looking to grow, scale, or restructure. Understanding the type of private equity fund, the size of the fund, and where a private equity fund is in its life cycle is important when considering a potential investment or acquisition proposal.

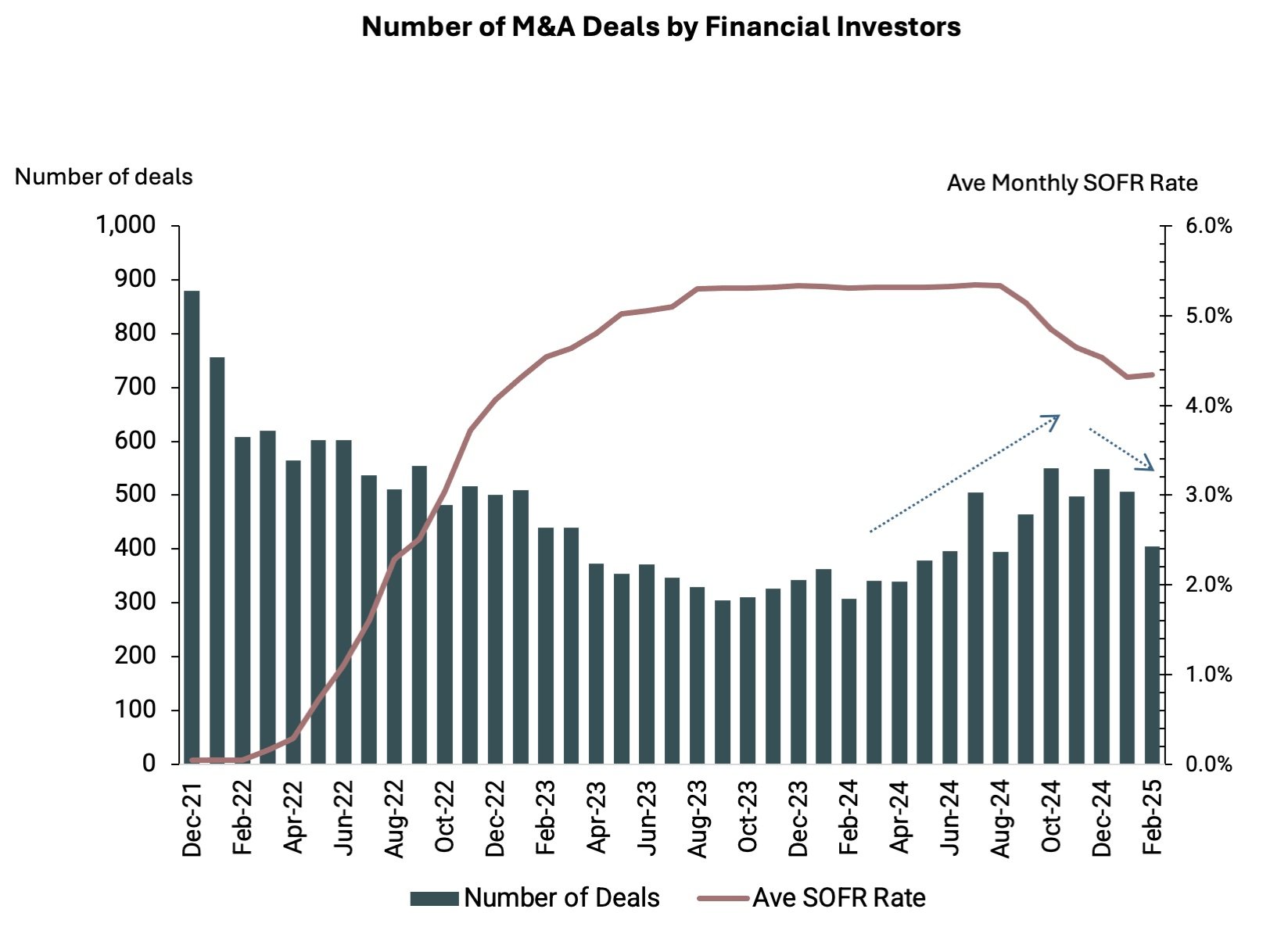

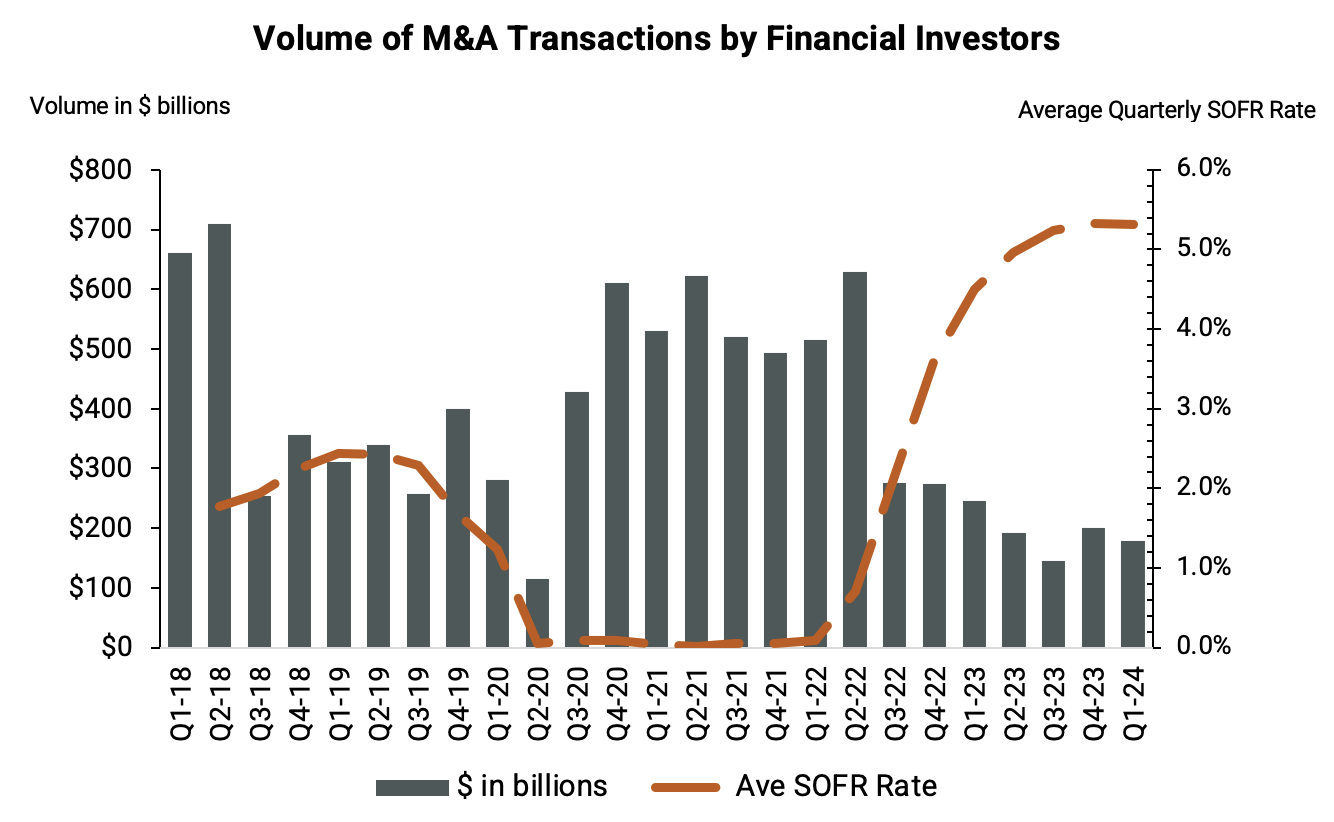

Q3-24: M&A Activity by Financial Investors Remains Down

Acquisition activity by private equity funds influence mergers and acquisitions (M&A) across many industries, but Q3-24 volume was down 64% from the peak. What does this mean for founder-owned and private companies who want to exit in 2025?

Top 10 Strategies to Generate Private Equity-like Returns

Private equity firms have a proven track record of delivering strong returns to investors and outperforming broader equity markets. But how do they do it? Check out our Top 10 Strategies for Founders, CEOs, and CFOs at private companies to drive stronger growth and value creation for their own shareholders.

How Changing Interest Rates Influence Mergers & Acquisitions by Financial Investors

Financial investors like private equity funds and venture capital firms help shape the market dynamics of mergers and acquisitions (M&A) across many industries. But as interest rates have risen precipitously since 2022, there has been a significant decline in the M&A activity among financial investors. What should companies do who are looking for an exit?

KKR’s Strategic Deal with Coty: Case Study

Overview of private equity firm KKR’s investment in global beauty company Coty. A look at private equity deal making amid COVID-19.